If you’re juggling high-interest credit card debt, every month you wait costs you money — sometimes a lot of money. At 24% APR, a $5,000 balance accumulates over $1,200 in interest every year, and that’s assuming you’re not adding to it. Balance transfer credit cards offer a genuine solution: move your existing debt to a new card with a 0% introductory APR period and pay it down without interest piling up. Here’s exactly how it works and how to use it strategically.

What Is a Balance Transfer and How Does It Work?

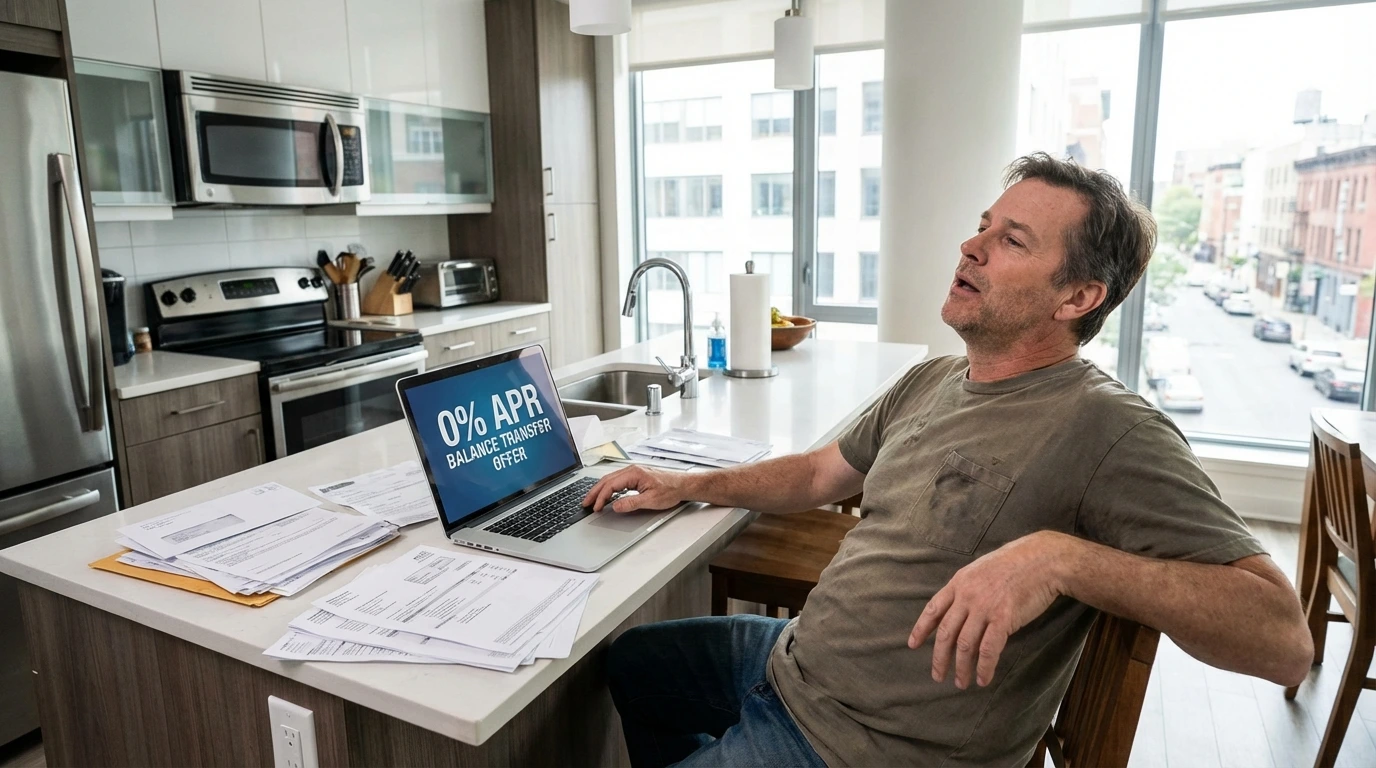

A balance transfer is simply the process of moving existing debt from one or more credit cards to a new credit card — usually one offering a promotional 0% APR period. During that promotional window, which typically lasts anywhere from 12 to 21 months, every payment you make goes entirely toward reducing your principal balance rather than paying interest.

The Basic Mechanics

Once you’re approved for a balance transfer card, here’s the typical process:

- You provide the account numbers and amounts you want to transfer

- The new card issuer pays off your old card(s) directly

- Your debt now sits on the new card at 0% APR

- You make monthly payments to the new card issuer

- After the promotional period ends, any remaining balance reverts to the card’s regular APR

The key is that step five — you need a realistic plan to pay off the transferred amount before the promotional period expires.

Why This Works So Well for Debt Payoff

Consider someone carrying $6,000 in credit card debt at 22% APR. Making a $300 monthly payment, they’d pay approximately $1,600 in interest over the payoff period. Transfer that same balance to a card with 0% APR for 18 months, and all $300 goes toward principal. The debt is gone in 20 months with zero interest paid (factoring in the transfer fee). The math is straightforwardly compelling for disciplined borrowers.

Who Benefits Most from Balance Transfers

Balance transfer cards work best for people who:

- Have a specific, manageable debt amount they can realistically pay off within the promo period

- Have good enough credit to qualify (typically 670+ FICO score)

- Are committed to not adding new purchases to the card

- Have stopped or plan to stop using the original high-interest cards

How to Maximize a 0% APR Offer

Getting approved for a balance transfer card is only the first step. To fully benefit from the offer, you need a clear repayment strategy from day one.

Calculate Your Required Monthly Payment

Take your total transferred balance, add the balance transfer fee, then divide by the number of months in the promotional period. That’s your target monthly payment. For example: $5,150 (including a 3% transfer fee on $5,000) divided by 18 months equals approximately $286 per month. Set up autopay for at least that amount so you never miss a payment.

Don’t Use the Card for New Purchases

This is critical and often misunderstood. Many balance transfer cards don’t extend the 0% rate to new purchases — those charges accrue interest at the regular APR immediately. Even worse, your payments may be applied to the 0% balance first, leaving new purchases accruing interest for months. Keep the balance transfer card exclusively for paying down your transferred debt.

Set Up Autopay Immediately

A single missed or late payment on most balance transfer cards triggers the penalty APR, which can be 29.99% or higher, and immediately cancels your promotional rate. Set up automatic minimum payments at a minimum, and ideally autopay for your full calculated monthly amount.

Track Your Payoff Progress

Put the promotional period end date in your calendar right now — not as a reminder a week before, but three months before. If you’re not on track to pay off the balance by then, you need to either increase your monthly payments or prepare for the balance to start accruing interest at the regular rate.

The Real Costs to Watch For

Balance transfers aren’t entirely free, and understanding the actual costs helps you evaluate whether the math works in your favor.

Balance Transfer Fees

Almost all balance transfer cards charge a fee of 3%–5% of the amount transferred, applied upfront. On a $5,000 transfer, that’s $150–$250 added to your balance immediately. This fee is almost always worth it compared to months of high-interest payments, but you need to factor it into your calculations:

- 3% fee on $5,000 = $150 added to balance

- 5% fee on $5,000 = $250 added to balance

- Compare this to the interest you’d pay staying on the original card

What Happens When the Promo Period Ends

If you still have a remaining balance when the 0% APR period expires, it immediately begins accruing interest at the card’s regular APR — which can be 19.99% to 29.99% depending on your creditworthiness. This is why having a concrete payoff plan before you transfer is so important. An incomplete payoff isn’t a failure, but you need to know the math ahead of time.

Impact on Your Credit Score

Applying for a balance transfer card creates a hard inquiry, temporarily lowering your score by a few points. Opening a new account also slightly reduces your average account age. However, the positive impact of lower credit utilization (as you pay down the transferred balance) typically outweighs these short-term effects within a few months.

Choosing the Right Balance Transfer Card

Not all balance transfer offers are created equal. Here’s what to evaluate when comparing your options.

Length of the Promotional Period

The longer the 0% APR window, the more flexibility you have. Cards offering 18–21 months give you significantly more breathing room than those offering 12 months. Match the promo length to how much you realistically need to pay off your balance:

- Under $3,000 in debt: A 12–15 month offer may be sufficient

- $3,000–$6,000 in debt: Look for 18-month offers

- Over $6,000 in debt: Target 20–21 month offers

The Balance Transfer Fee

Prioritize cards with a 3% transfer fee over 5% if you’re transferring a large balance. Some cards occasionally offer a limited-time 0% transfer fee promotion, which is worth watching for if you’re not in a rush. However, a slightly higher fee is usually worth it to access a longer promotional window.

Regular APR After the Promo Period

Compare the ongoing APR in case you don’t pay off the full balance in time. A card with a slightly shorter promo period but a lower ongoing APR may be better if you anticipate carrying a small remainder.

Whether the Card Has Additional Value

Some balance transfer cards also earn rewards or cashback, which can be useful once your debt is paid off. However, don’t choose a card based primarily on rewards when your immediate goal is debt elimination — prioritize the transfer terms and payoff math first.

Conclusion

Balance transfer cards are one of the most powerful tools available for eliminating credit card debt faster and cheaper. By moving high-interest balances to a 0% APR card and committing to a disciplined monthly payment plan, many Americans have paid off thousands of dollars in debt without paying a cent in interest. The key elements of success are simple: calculate your required monthly payment before you transfer, set up autopay, avoid new purchases on the card, and pay off the full balance before the promotional period ends. With the right card and a clear plan, you can turn a stressful debt situation into a manageable, interest-free payoff timeline.

Read more at https://en.icardin.com/