Most people who try to pay off debt fail — not because they lack willpower, but because they lack a plan. Vague intentions like “I’ll pay more this month” or “I’ll get serious after the holidays” don’t stand up to real life. What works is a specific, written debt payoff plan with clear targets, a defined method, and a tracking system that keeps you motivated through the hard months. Whether you owe $5,000 or $80,000, the same framework applies. This guide walks you through how to build a debt payoff plan that’s realistic, strategic, and actually designed to succeed.

Map Out All Your Debt

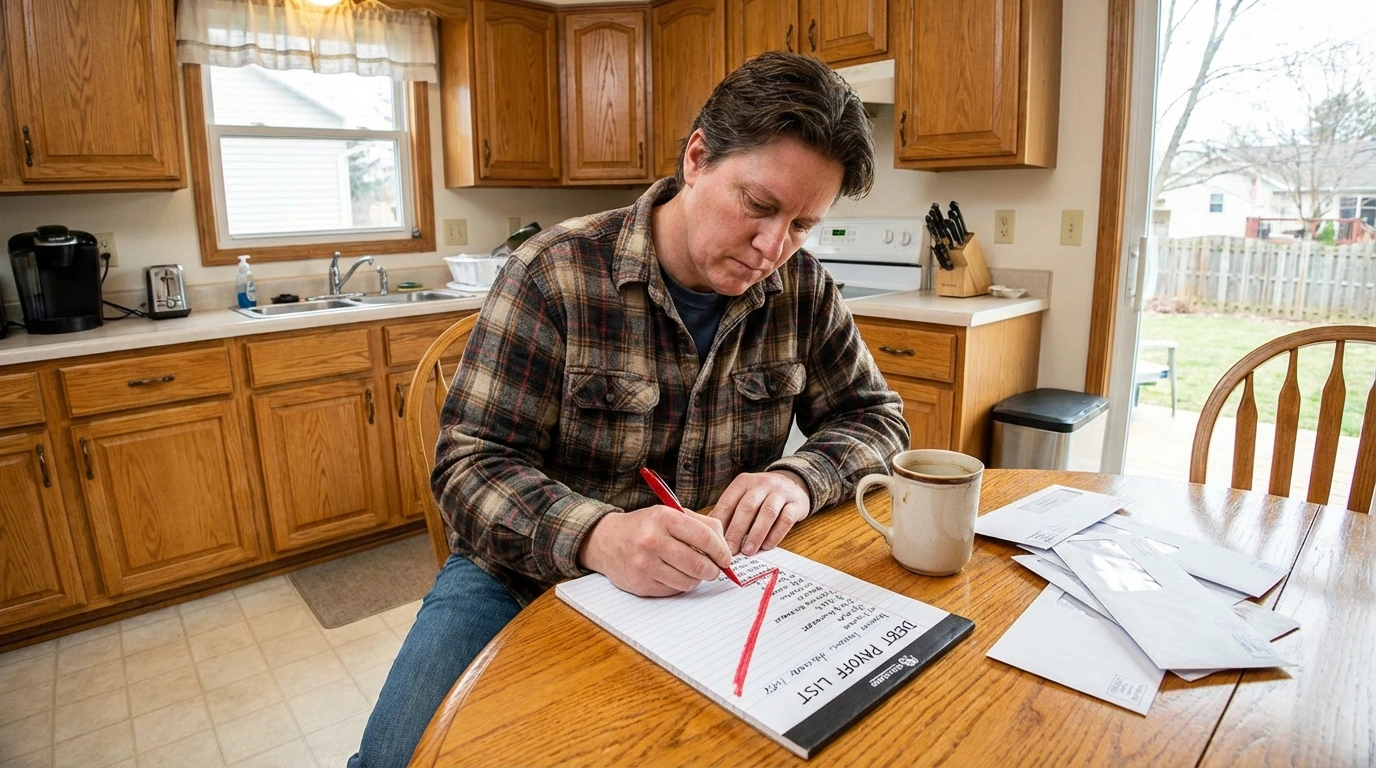

You cannot make a plan until you know exactly what you’re working with. This step is uncomfortable for many people, but it’s the foundation of everything that follows.

Create Your Debt Inventory

List every single debt you carry. Pull out credit card statements, loan agreements, and your most recent statements. For each debt, record:

- The creditor name

- Current balance

- Interest rate (APR)

- Minimum monthly payment

- Due date

Organize this in a simple spreadsheet or on paper. This master list is your starting point and your scorecard.

Calculate Your Total Debt Load

Add up all balances. Many people are shocked by the total — and that shock can be motivating. If you owe $34,000 across six accounts and were thinking of it as “just some credit card debt,” seeing the real number changes your relationship with the problem.

Understand the True Cost of Your Debt

High-interest credit card debt at 22% APR is genuinely expensive. On a $5,000 balance, paying only the minimum could take 15+ years and cost you $7,000 in interest alone. Use a debt payoff calculator to see what each debt actually costs over time. Understanding this urgency helps you stay committed when motivation dips.

Choose Your Payoff Strategy

There are two dominant debt payoff strategies, each with different strengths. Understanding both helps you choose the one that fits your psychology and financial situation.

The Debt Avalanche Method

With the avalanche method, you pay minimum payments on all debts, then throw every extra dollar at the highest-interest debt first. Once that’s paid off, you roll its payment to the next highest-rate debt, and so on. Mathematically, this is the optimal approach — it minimizes the total interest you pay and gets you out of debt fastest. If you’re motivated by logic and long-term efficiency, this is your method.

The Debt Snowball Method

With the snowball method, you pay minimums on all debts but put extra money toward the smallest balance first, regardless of interest rate. When that debt is wiped out, you roll its payment to the next smallest. Research by Harvard Business School found that people who use the snowball method are more likely to stick with their plan and eliminate debt completely — because the early wins build momentum and confidence. If you’ve struggled with debt payoff before, the snowball’s psychological power may be worth the small mathematical cost.

Hybrid Approaches

Some people start with the snowball to build confidence, then switch to avalanche once they’ve eliminated two or three accounts and feel psychologically locked in. Others use a hybrid based on their specific debt mix — for example, eliminating a $300 medical bill quickly (snowball) before tackling $18,000 in student loans at 6.5% vs. $15,000 in credit card debt at 24% (avalanche from there).

- Avalanche: mathematically optimal, best for disciplined planners

- Snowball: psychologically powerful, best for those who’ve struggled before

- Choose one method and stick with it — consistency beats optimization

Find Money to Accelerate Payoff

A solid strategy with minimal extra payment still takes years. Finding additional money to throw at your debt is the accelerant that makes the plan work faster.

Audit Your Monthly Spending

Go through three months of bank and credit card statements and categorize every expense. Most people find at least $100-$300 in spending that isn’t providing real value — subscriptions they forgot about, dining out frequency, convenience purchases. Redirect that money to debt. Even $150 per month extra, applied consistently to a $10,000 balance at 20%, cuts years off your payoff timeline.

Increase Your Income

Cutting expenses has a ceiling — you can’t cut below zero. But income has no ceiling. Consider:

- Asking for a raise or seeking a higher-paying job

- Freelancing or consulting in your field on evenings and weekends

- Selling unused items (furniture, electronics, clothes) for lump-sum payments

- Renting out a room, parking space, or storage area

- Driving for a rideshare app, doing gig work, or seasonal part-time work

Committing 100% of any additional income to debt payoff for the duration of your plan is a powerful rule. It prevents lifestyle inflation from absorbing your extra earning power.

Lower Your Interest Rates

Before assuming your interest rates are fixed, explore options to reduce them. Balance transfer credit cards with 0% promotional APRs (12-21 months) can eliminate interest on transferred balances during the promo period, but read the terms carefully for transfer fees and what happens after the promo expires. Personal loans at lower rates can consolidate high-interest credit card debt. Even calling your credit card company and asking for a rate reduction works — especially if you’ve been a long-term customer with a good payment history.

Build Systems That Keep You on Track

Motivation is unreliable. Systems are not. The difference between people who pay off debt and people who don’t is rarely willpower — it’s whether they built structures that make progress automatic.

Automate Minimum Payments

Set up autopay for the minimum payment on every account, every month. This protects your credit score and ensures you never get hit with a late fee or penalty APR. Then make your extra, debt-attack payment manually to whichever account you’re targeting. Separating these two actions keeps you intentional about where your extra money is going.

Track Your Progress Visually

A visual debt tracker — a simple chart or spreadsheet you update monthly — has an outsized motivational effect. Seeing the bars drop, the totals decrease, and the paid-off accounts pile up creates a feedback loop that reinforces your effort. Some people color in a visual “thermometer” chart; others use a spreadsheet that auto-calculates their debt-free date as balances decrease.

Celebrate Milestones Without Sabotaging Progress

Plan small celebrations for specific achievements: paying off your first account, hitting 25% paid off, the halfway mark. These celebrations should be modest (a dinner out, not a vacation) and pre-planned so they don’t become a rationalization for overspending. Acknowledging progress keeps you psychologically engaged for the long haul.

- Set a specific, written debt-free target date

- Review your plan monthly and adjust for changes in income or expenses

- Find an accountability partner or online community for support

- Keep your debt inventory updated in real-time so the progress is always visible

Conclusion

A debt payoff plan that actually works isn’t complicated — but it does require honesty, commitment, and structure. Start by facing the full reality of what you owe. Choose an attack method that fits your psychology, whether that’s the mathematically superior avalanche or the motivationally powerful snowball. Find every possible dollar to redirect toward debt. And build automated systems with visual tracking to make progress feel real and sustainable. Getting out of debt takes time — months or years, not weeks — but each payment moves you closer to a financial life with more freedom and less stress. Build the plan, trust the process, and the debt-free finish line will come.

Read more at https://en.icardin.com/